Cryptocurrency Withdrawal Tax Strategies: What Works

The world of cryptocurrency has taken the financial industry by storm, with millions of individuals and institutions investing in digital currencies like Bitcoin, Ethereum, and more. However, one aspect that is often overlooked or misunderstood is the tax obligations when it comes to withdrawing funds from these cryptocurrencies. The IRS and other governments have implemented various regulations to ensure compliance with tax laws, but not all cryptocurrency holders know how to navigate the complex web of tax rules.

In this article, we will explore the different tax strategies for cryptocurrency withdrawals and what works best for individuals and businesses in the digital currency space.

Understanding Tax Obligations

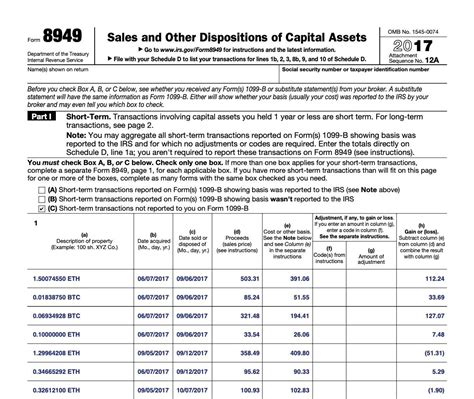

The Internal Revenue Service (IRS) defines a taxable event as any transaction involving a financial activity that is considered taxable to the recipient. In the case of cryptocurrencies, this includes sales, exchanges, or other transactions in which an individual or entity sells or receives digital assets for consideration.

To avoid paying taxes on your cryptocurrency earnings, it is essential to understand how to report these transactions and what tax strategies are available. Here are some key concepts to keep in mind:

- Capital Gains Tax: If you sell cryptocurrency at a profit, the gain is subject to capital gains tax rates, which can range from 0% to 20%.

- Taxable Transactions: Cryptocurrency transactions that are not considered taxable are generally exempt, such as:

- Trading between individuals or small businesses for personal use.

- Buying and selling cryptocurrency for personal investment purposes.

- Receiving cryptocurrency as compensation for work or services.

Tax Strategies for Withdrawals

To minimize your tax liability on cryptocurrency withdrawals, consider the following strategies:

- Holding Period: Keep track of how long you have held the cryptocurrency. This can impact your capital gains tax rate and the timeframe within which you are eligible to sell.

- Tax Loss Harvesting: If you have incurred losses on other investments or assets, consider using them to offset gains on your cryptocurrency transactions.

- Tax Efficient Investments: Consider investing in cryptocurrencies that are more liquid and have lower capital gains tax rates, such as Bitcoin.

- Self-Directed IRAs (Individual Retirement Accounts): Self-directed IRAs allow individuals to hold alternative assets, including cryptocurrency, within a retirement account.

Practical Examples

To illustrate how these strategies work in practice, consider the following examples:

- A self-employed individual selling cryptocurrency for personal use could report the earnings on Schedule C and claim a deduction for business expenses.

- If you transact between individuals or small businesses for personal use, your capital gains tax rate may be lower than if you sold directly from your account.

Ultimately, understanding the complex tax rules surrounding cryptocurrency withdrawals is key to maximizing your tax benefits. By applying these strategies and staying informed about changing tax laws, individuals in the digital currency space can minimize their tax liability while continuing to grow their wealth.

Additional Resources

For more information on tax regulations and strategies specific to cryptocurrency investors, see the following resources:

- IRS Publication 265 (Tax Treatment of Certain Capital Gains and Losses)

- Section 199A of the Tax Cuts and Jobs Act (TCJA)

- SEC Rule 34 (Reporting of Securities Transactions)

Stay informed about evolving tax laws and regulations in the cryptocurrency industry.